Oklahoma: Texas Speed Without Texas Congestion

There is a reason so much of the data center conversation still revolves around Texas. It offers speed, scale, and a regulatory environment that has historically allowed projects to move quickly. For years, that combination made it one of the most attractive markets in the country.

But speed without predictability has started to create friction.

ERCOT has delivered rapid growth, but it has also introduced uncertainty around interconnection timelines, grid stability, and long-term planning. And when a market begins to feel unpredictable, demand does not disappear. It looks for the closest alternative that can offer similar advantages with fewer surprises.

The Alternative Next Door

That alternative is Oklahoma.

This is not a market trying to replicate Texas. It is a market benefiting from Texas. At the center of this shift is OG&E, which is increasingly part of conversations that would have previously been confined to Dallas or other Texas hubs.

Oklahoma offers a version of the Texas proposition with a different risk profile. It provides access to power, available land, and a central location, but with a perception of greater stability.

Who Is Actually Moving

The buyers entering Oklahoma are not random. They are the ones most sensitive to delays and unpredictability.

Enterprise colocation users who have faced congestion in Dallas are beginning to look outward. Firms that expected to deploy quickly in Texas are reassessing timelines and searching for alternatives that can deliver more consistent outcomes.

AI startups and emerging compute companies are also part of this movement. Many of them were drawn to Texas for its speed, but are now weighing that speed against the risks of delay. Hyperscaler overflow is another piece of the story, as companies like Amazon Web Services and Google explore capacity beyond their core Texas footprints.

Stability Becomes the Product

What unites these buyers is a shift in what they value. Speed still matters, but predictability is becoming just as important.

They want to move quickly, but they also want to know that their timelines will hold. That combination is not always guaranteed in Texas today.

Oklahoma offers a different balance. It may not have the same scale or brand recognition, but it provides a level of consistency that is becoming increasingly attractive.

The Constraints Are Subtle

Oklahoma’s limitations are not immediately visible, but they are real.

Perception is one of the biggest hurdles. It is still not widely viewed as a primary data center market, which affects how quickly capital and tenants move. The ecosystem is also less developed, with fewer existing hyperscale campuses and a smaller network of experienced vendors and operators.

This does not prevent growth. It slows recognition.

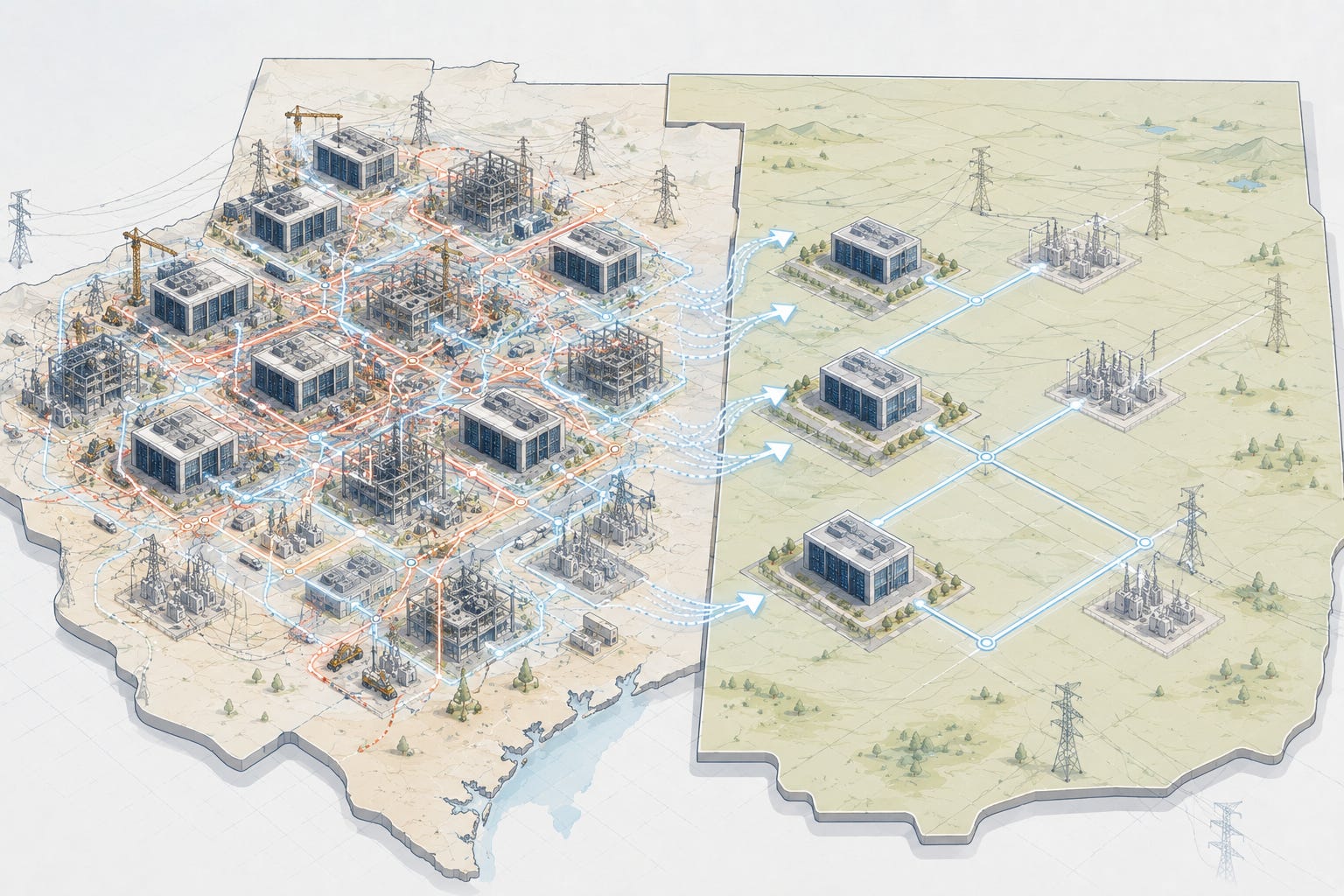

Where the Market Is Forming

Oklahoma County, centered around Oklahoma City, is emerging as the primary hub. Its central location and existing infrastructure support deployments in the 20 to 40 megawatt range. This is where the majority of initial activity is concentrating.

Canadian County, just to the west, offers a natural expansion corridor. With available land and room to scale, it supports 20 megawatt deployments that build on the core market.

Tulsa County represents a secondary node. It serves regional demand and supports projects in the 10 to 30 megawatt range. This is a mid-cycle market that grows as the broader ecosystem expands.

Spillover Without the Chaos

For developers, the opportunity in Oklahoma is tied directly to what is happening in Texas. This is not about creating demand from scratch. It is about capturing demand that is looking for an alternative.

The advantage is not just cost. It is the ability to deliver projects with fewer disruptions. That becomes a differentiator when timelines are critical.

For capital, Oklahoma represents an undervalued position in the Midwest and Southern corridor.

Pricing has not yet fully adjusted to the level of demand that is beginning to move into the state. Investors who recognize the spillover dynamic can position themselves ahead of broader market awareness.

As more projects are announced and completed, that gap is likely to narrow.

For operators, Oklahoma offers something increasingly rare. It offers the ability to plan with a higher degree of confidence.

Projects can be structured around timelines that are more likely to hold. That does not eliminate risk, but it changes the nature of it.

The Real Takeaway

Oklahoma is not competing with Texas. It is complementing it.

And as ERCOT continues to balance speed with complexity, the markets that can offer a more predictable path will quietly become some of the most important in the next phase of data center development.

PLUS: If you want to go deeper:

1. Sanity check a deal

If you’re looking at a site, interconnection path, or development opportunity and something doesn’t fully add up, reply and share it. I review a small number each week and break down what actually matters.

2. Figure out where you fit

If you’re trying to understand how to access real deal flow in this space, reply with “Positioning” and a few lines about your background. I’ll map where you realistically plug in.

3. Work together

If you’re actively pursuing sites or investments and want a clearer strategy around power, siting, and timing, reply with “Work Together” and what you’re working on.