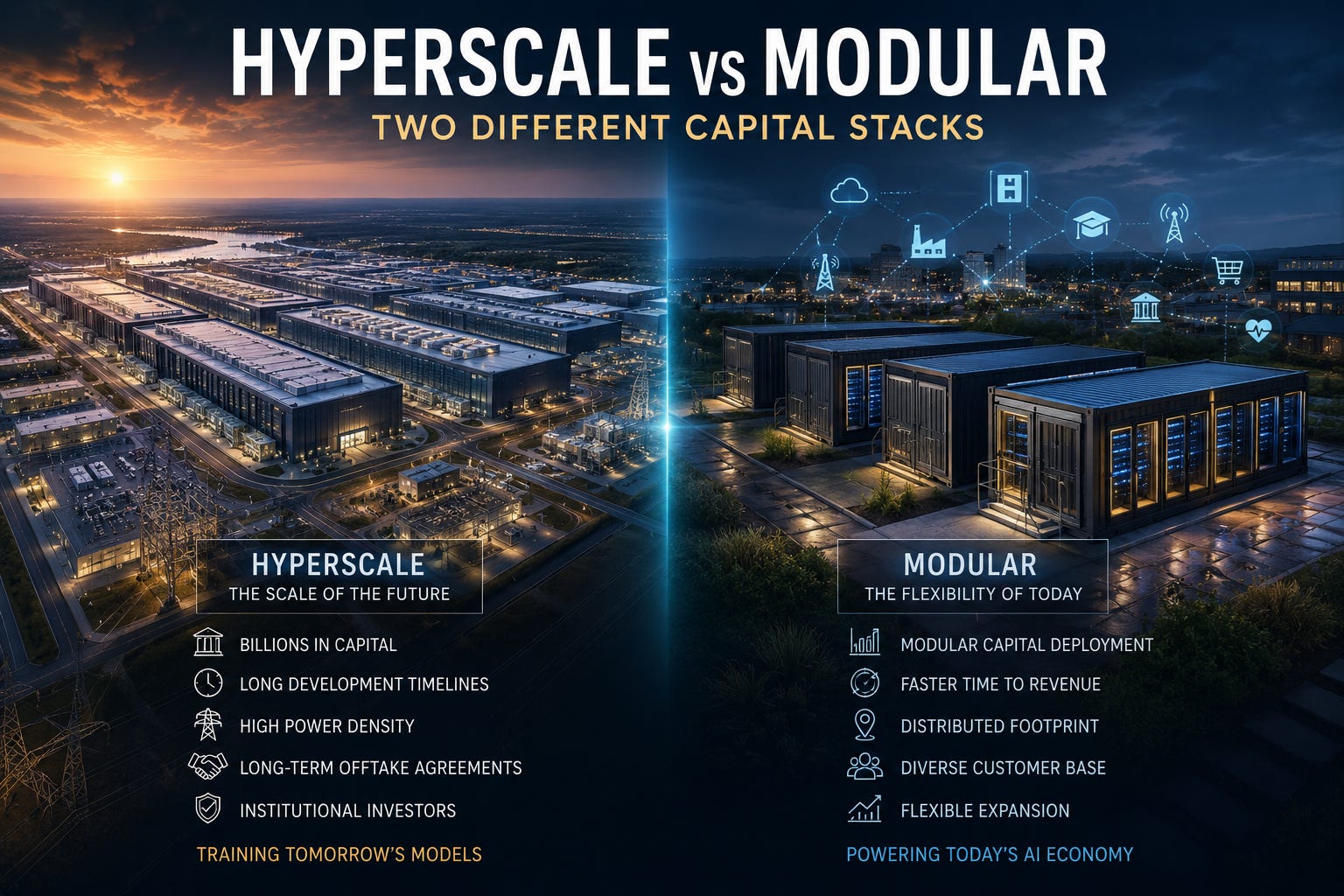

Hyperscale vs. Modular: Two Different Capital Stacks

The AI infrastructure conversation often assumes that every data center project is competing in the same market.

That assumption is becoming increasingly difficult to defend. As AI infrastructure expands, the industry is not simply becoming larger. It is becoming more specialized. Different workloads require different deployment strategies, different infrastructure designs, and increasingly, different sources of capital.

This distinction is beginning to reshape the economics of digital infrastructure.

When investors discuss AI data centers, they often envision billion-dollar hyperscale campuses consuming hundreds of megawatts of electricity. At the same time, another market is quietly emerging around modular deployments, retrofit facilities, and regional inference infrastructure measured in megawatts rather than gigawatts. Both markets are growing rapidly, but they are governed by very different financial models.

Understanding those differences is becoming increasingly important for developers, investors, and policymakers alike.

Not Every Megawatt Requires the Same Capital

One of the biggest misconceptions in today’s market is that AI infrastructure represents a single asset class.

It does not.

A hyperscale campus designed to support frontier model training bears little resemblance to a modular facility serving regional healthcare systems, manufacturers, universities, or enterprise AI workloads. The physical buildings may look similar, but the underlying economics often differ substantially.

Scale changes almost everything.

Larger campuses require significant upfront land acquisition, transmission planning, utility coordination, specialized networking, and power infrastructure that may take years to develop. These projects frequently involve billions of dollars in capital and extended development timelines before generating meaningful revenue.

Modular deployments follow a different path.

Rather than waiting for a single large project to reach completion, operators can deploy capacity incrementally as demand grows. This reduces initial capital requirements while allowing revenue generation to begin much earlier in the development cycle.

The result is a fundamentally different investment profile.

The Economics of Hyperscale

Hyperscale development rewards long-term capital.

Investors financing these projects understand that value creation depends on assembling enormous infrastructure systems before customers begin consuming compute. Land must be secured, substations constructed, transmission upgrades coordinated, and power infrastructure energized long before GPU clusters become operational.

This naturally attracts investors comfortable deploying large amounts of capital over extended time horizons.

Infrastructure funds, sovereign wealth funds, pension funds, insurance companies, and major institutional investors increasingly fit this profile. They seek predictable long-term returns from assets capable of supporting decades of economic activity.

The investment thesis resembles large transportation, energy, or utility infrastructure projects more than conventional commercial real estate.

Patience becomes part of the strategy.

The Economics of Modular Infrastructure

Modular infrastructure rewards flexibility.

Instead of committing enormous amounts of capital at the beginning of a project, developers can expand capacity in stages as customer demand evolves. Capital expenditures become more closely aligned with actual utilization rather than projected utilization several years into the future.

This creates opportunities for a different group of investors.

Growth equity firms, private developers, specialized infrastructure operators, regional investment groups, and strategic corporate investors may find modular deployments more attractive because capital can be deployed in smaller increments while maintaining flexibility as technology evolves.

The investment horizon often becomes shorter.

Revenue can begin earlier, expansion decisions remain optional, and facilities can adapt more easily as hardware generations, cooling technologies, and customer requirements continue changing.

Risk Is Allocated Differently

The distinction between these two markets extends beyond project size.

It changes how risk is distributed throughout the development process.

Hyperscale projects concentrate risk at the beginning of the investment cycle. Developers must make significant commitments regarding power procurement, transmission planning, site design, and customer demand years before facilities become operational. Success depends on accurately anticipating long-term market conditions.

Modular infrastructure distributes risk over time.

Operators retain the ability to expand, pause, or modify deployments as market conditions evolve. Rather than committing to a single large buildout, they continuously adjust investment decisions based on actual demand and technological change.

Neither approach is inherently superior.

Each solves a different infrastructure problem.

Different Customers Create Different Capital Structures

Capital ultimately follows customers.

Hyperscale facilities primarily serve cloud providers, frontier AI developers, and organizations requiring enormous concentrations of computational power. These customers often negotiate long-term commitments capable of supporting large infrastructure investments.

Modular deployments frequently serve a broader customer base.

Regional enterprises, healthcare systems, universities, manufacturers, telecommunications providers, logistics operators, and government agencies may require localized AI infrastructure without needing hundreds of megawatts of capacity. Their requirements often favor flexibility, geographic proximity, and incremental expansion rather than maximum scale.

Different customers naturally produce different financing structures.

The infrastructure simply follows demand.

Why This Matters for Investors

Many investors continue evaluating AI infrastructure through a single lens.

That approach increasingly overlooks the diversity emerging across the sector.

The future AI infrastructure economy may include multiple capital markets operating simultaneously. One market finances nationally significant hyperscale campuses requiring billions of dollars and decades of operational planning. Another finances distributed networks of modular facilities serving regional inference, enterprise AI, and operational computing needs.

These markets are complementary rather than competitive.

Training large models requires extraordinary scale. Deploying those models throughout the broader economy increasingly requires distributed infrastructure located closer to users, enterprises, and operational systems.

Both layers create investment opportunities.

They simply require different financial tools.

A More Fragmented Infrastructure Economy

The data center industry is entering a period of increasing specialization.

Developers will continue building massive hyperscale campuses that anchor the next generation of AI training infrastructure. At the same time, modular deployments, retrofit facilities, and distributed compute systems will continue expanding as AI becomes embedded throughout healthcare, manufacturing, education, finance, telecommunications, and public infrastructure.

These are not different versions of the same business.

They represent different infrastructure ecosystems with different customers, different deployment strategies, different operating models, and increasingly, different capital stacks.

Recognizing that distinction helps explain why the future of AI infrastructure will not be dominated by a single development model.

The industry is not simply growing larger.

It is becoming more financially sophisticated.

As AI infrastructure continues maturing, understanding how capital flows through these different layers may become just as important as understanding where the next megawatt of power will be built.

PLUS: If you want to go deeper:

1. Pressure test a site or opportunity

Looking at a site, powered land opportunity, or development project? If something doesn’t fully add up, reply and share it. I review a small number each week and break down the assumptions, risks, and bottlenecks that matter most.

2. Figure out where you fit

Trying to access real opportunities in digital infrastructure? Reply with “Positioning” and a few lines about your background. I’ll share where I think your skills are most likely to create leverage.

3. Explore a project together

If you’re actively pursuing sites, investments, or infrastructure opportunities and want a clearer framework around power, demand, approvals, and timing, reply with “Work Together” and a brief description of what you’re evaluating.